Show Menu

Menu

Categories

Books

Crafts & Entertaining

Food & Recipes

Money & Finance

Life

Home & Organization

Parenting & Family

About

Contact

Recent

Search Results : new-ways-to-save

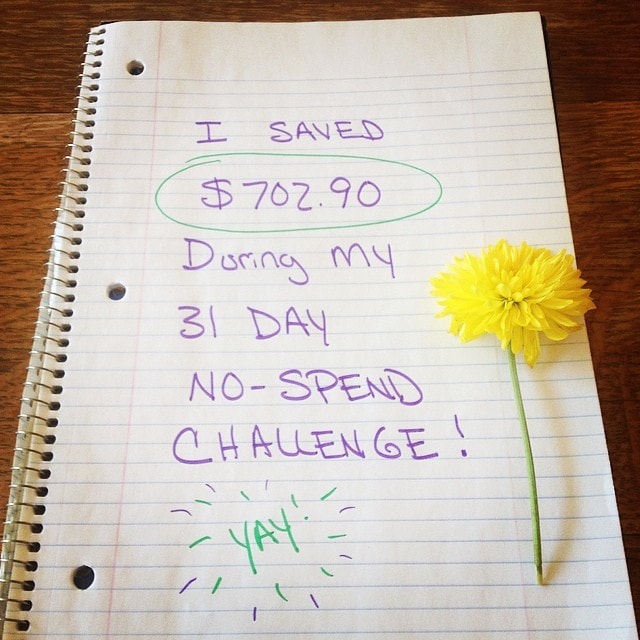

Reader Transformation: Shanna’s No Spend Challenge

Reducing Expenses: Put the ‘Personal’ In Your ...

New Ways to Save in the New Year