Show Menu

Menu

Categories

Books

Crafts & Entertaining

Food & Recipes

Money & Finance

Life

Home & Organization

Parenting & Family

About

Contact

Recent

Search Results : month-of-savings

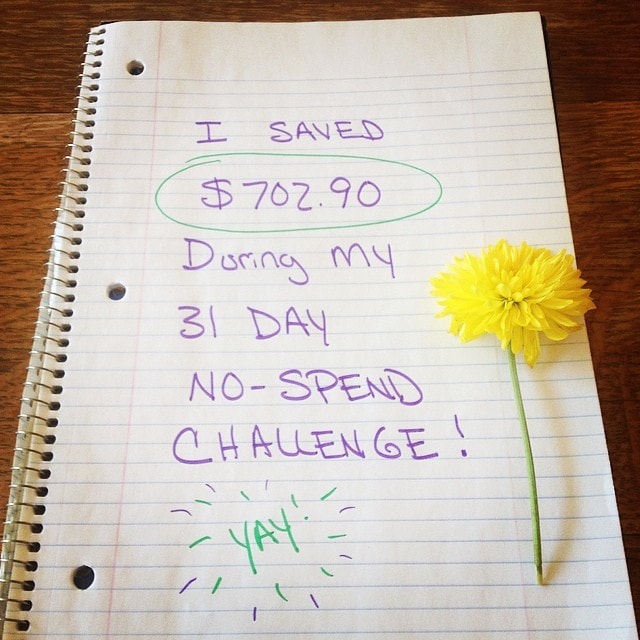

Reader Transformation: Shanna’s No Spend Challenge

Day 30: Life’s Great Lessons

Day 29: Get Rewarded For Your Shopping

Day 28: Get To Know Your Freezer

Day 27: Save on Clothing

Day 26: Extending It Further

Day 25: Schedule a Day in Your Kitchen

Day 24: Become a Coupon Queen (or Not)

Day 23: Just Ask

Day 21: Create Your Own Secret Emergency Account

Day 20: Curb Your Weekend Spending

Even More Results